Insurance has always had a back room. The customer sees a policy. The agency sees applications, estimates, invoices, renewals, comparison records, intention-confirmation notes, corporate contracts, insurer portals, and a long chain of human checks that rarely become visible until something goes wrong.

On June 1, 2026, justInCaseTechnologies announced that it wants to put an AI agent into that back room. Its new service for corporate insurance agencies is not being sold as a mere chatbot. The company describes it as a next-generation solution in which AI takes the lead in completing back-office operations, supported by an AI processing platform and specialist staff.

The timing matters. Japan’s revised Insurance Business Act took effect in June 2026, adding pressure around business quality, governance, comparison recommendations, customer-intention confirmation, and recordkeeping. For corporate agencies already facing staff shortages and the retirement of experienced workers, the compliance burden is becoming an operational problem. justInCaseTechnologies is trying to turn that problem into an AI-agent workflow.

What was announced

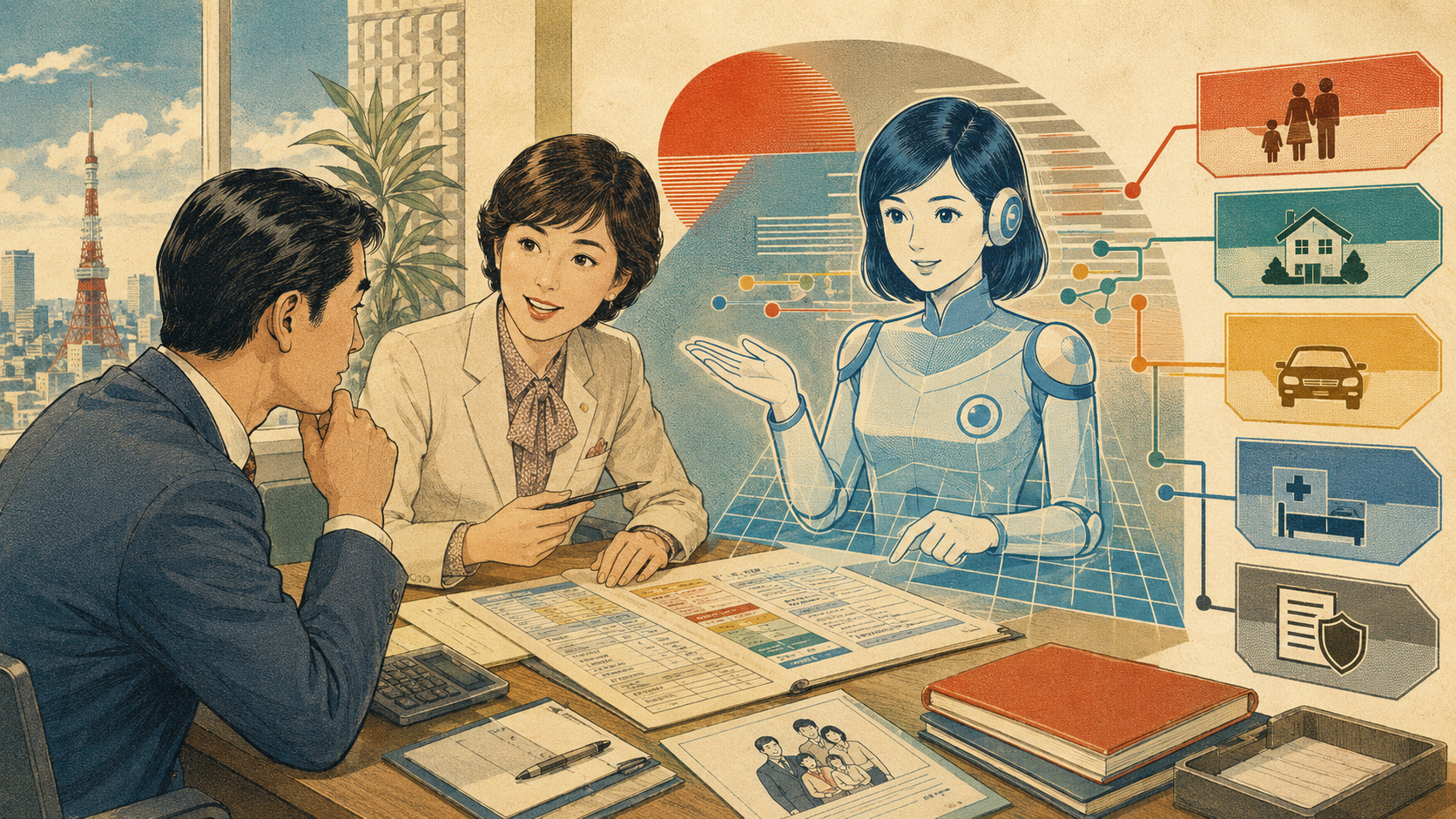

The service has three pillars. First, AI-led completion of back-office work: the company receives corporate-agency operations and uses its own AI processing base to handle work from application intake to data entry, checking, and document issuance. Second, a customization phase: after operations are standardized through BPO, the knowledge can be reflected into a client-specific AI agent. Third, the company emphasizes financial-grade information security and audits under an ISMS-based policy.

Two ready-to-use agents are positioned at the center. The first is an insurance AI agent for agency systems. It supports links with insurer systems, reduces the work required to create estimates, and supports the strengthened process around comparison recommendations and customer-intention confirmation, including the creation of recommendation-reason records. The second is an insurance AI agent for corporate contracts. It assists with complex questionnaires, document checks, missing entries, and consistency review.

Why corporate agencies are the right battlefield

Corporate insurance agencies sit in a difficult place. They are not only sales channels. They often handle group companies, employees, business partners, benefit programs, renewals, and corporate insurance arrangements that involve more than one insurer and more than one internal stakeholder.

That makes the work operationally heavy. A corporate agency must understand customer needs, compare products, record the reason for recommendations, coordinate across insurer systems, and manage corporate documents. When an experienced worker leaves, the loss is not just a labor gap. It is a loss of tacit knowledge: where to click, what to check, which exception matters, which insurer’s portal behaves differently, and how to leave a defensible record.

AI agents are attractive because the problem is not only “too much paperwork.” The deeper problem is that the paperwork contains rules, sequences, exceptions, and judgment points. A general-purpose chatbot can answer a question. A useful insurance agent must move through a workflow, check facts, preserve logs, and know when a human expert must verify the result.

The long history behind Japan’s insurance back office

Japan’s modern insurance industry grew alongside the Meiji state and modern capitalism. Tokio Marine was founded in 1879 with encouragement from Eiichi Shibusawa, and early clients included major trading and shipping interests. Meiji Life followed in 1881, and Nippon Life was established in 1889. Insurance became part of the infrastructure of industrial Japan: shipping, factories, urbanization, households, health, life, and disaster risk all required ways to calculate, pool, and record uncertainty.

From the beginning, insurance was not only a product. It was a recordkeeping system. Policies, rates, actuarial assumptions, claims files, agency networks, sales conduct, and reinsurance arrangements all depended on trust in process. A promise to pay in the future is only valuable if the records of the past are accurate.

That is why insurance has often been slow to modernize. Digital application forms, embedded insurance, small-amount and short-term insurance, insurance SaaS, and mobile-first products all changed parts of the customer experience. But the industry’s core obligation remained the same: explain the product, understand the customer’s intent, maintain records, and pay claims when conditions are met. AI is now entering this older structure.

From justInCase to justInCaseTechnologies

The justInCase story began in 2016. Before founding the company, CEO Kazy Hata worked as an actuary in reinsurance product development and saw two major obstacles: regulatory approvals and legacy IT systems. With cloud computing and new software architectures advancing, the founding question was simple but radical for Japanese insurance: could technology make product development and delivery faster?

justInCase was first established to develop insurance products. Two years later, justInCaseTechnologies was founded to focus on system development. Its SaaS-based insurance system, joinsure, was adopted by clients including electric power companies and card companies. Celent has also identified Joinsure as an insurance SaaS supporting insurance DX in Japan’s insurtech landscape.

By 2026, the company was moving beyond insurance SaaS into generative AI. FinTech Observer reported that the joinsure AI Insurance Sales Enablement Series was designed to attack digital-application drop-off, with pilots at Kansai Electric Power and UCS reportedly delivering conversion-rate increases of up to 35 percent versus pre-implementation levels. The new corporate-agency AI agent takes that AI direction into the less glamorous but more durable world of agency operations.

The agentic shift: from forms to execution

The word “agent” matters. In 2023, many companies understood generative AI as a writing or answering machine. By 2026, the conversation has shifted toward systems that can take steps: read documents, check records, fill fields, compare conditions, ask for missing information, call external systems, and leave an audit trail.

Insurance is a natural test case for that shift. A good agency workflow is already agent-like. It has inputs, rules, exceptions, outputs, and escalation points. It is repetitive enough for automation, but regulated enough that unsupervised automation is dangerous. That is why justInCaseTechnologies’ model pairs AI automation with specialist double-checking rather than presenting the system as a fully autonomous replacement for human responsibility.

The best version of this technology would not remove accountability. It would make accountability easier: consistent records, cleaner comparisons, fewer missing fields, faster invoice issuance, and a clearer distinction between routine work and judgment-heavy work.

What could go wrong

The risks are real. Insurance data can include sensitive personal and corporate information. If AI agents connect with insurer systems, agency systems, and document workflows, security becomes a design requirement rather than an afterthought. Logs must be clear. Access rights must be controlled. Errors must be traceable.

There is also a governance risk. If employees trust the agent without understanding its limits, the system could standardize mistakes at scale. If the system is too rigid, it may fail to capture real customer nuance. If it is too flexible, it may create inconsistent recommendations. Insurance AI must live inside rules, not around them.

Finally, there is a cultural problem. The most valuable knowledge inside an agency often belongs to veteran workers who have spent years learning exceptions. AI adoption will work best when those workers are treated as teachers of the system, not as obstacles to be replaced.

Reader’s guide

| Question | Answer |

|---|---|

| What happened? | justInCaseTechnologies launched an AI agent service for corporate insurance agencies. |

| What does it do? | It supports back-office workflows including application intake, data entry, checks, document issuance, estimates, invoices, and corporate-contract review. |

| Why now? | Japan’s revised Insurance Business Act took effect in June 2026, while agencies face staff shortages and loss of veteran know-how. |

| What is the model? | Begin with AI-assisted BPO, standardize operations, and then build client-specific AI agents as internal assets. |

| What is the big question? | Can AI improve speed and continuity while strengthening, not weakening, explanation, recordkeeping, and governance? |

Japan.co.jp view

This is one of the more interesting small-company AI stories because it is so practical. There is no grand artificial-general-intelligence claim here. There is an agency desk, a quote, a missing field, a comparison record, a revised law, and a worker who may retire next year.

If AI changes Japan, it will not only happen in robotics labs or semiconductor fabs. It will happen in administrative rooms where expert clerical knowledge has quietly held industries together for decades. Insurance is a good place to watch because trust is not optional. AI can only win here if it makes the record more reliable.

For justInCaseTechnologies, the corporate-agency AI agent is more than another product. It is a test of whether Japan’s insurtech movement can move from selling digital insurance to rebuilding the infrastructure underneath insurance work itself.

Sources and references

This article used justInCaseTechnologies’ official release and company-history materials, FinTech Observer, Celent, Nippon Life, and insurance-history references.

- PR TIMES / justInCaseTechnologies: Launch of the AI agent service for corporate insurance agencies, June 1, 2026.

- justInCaseTechnologies: Company history and founding background.

- FinTech Observer: joinsure AI Insurance Sales Enablement Series and conversion-rate pilot context.

- Celent: Insurtech in Asia Series: Japan.

- Nippon Life: Our History.

- Swiss Re: A History of Insurance in Japan.