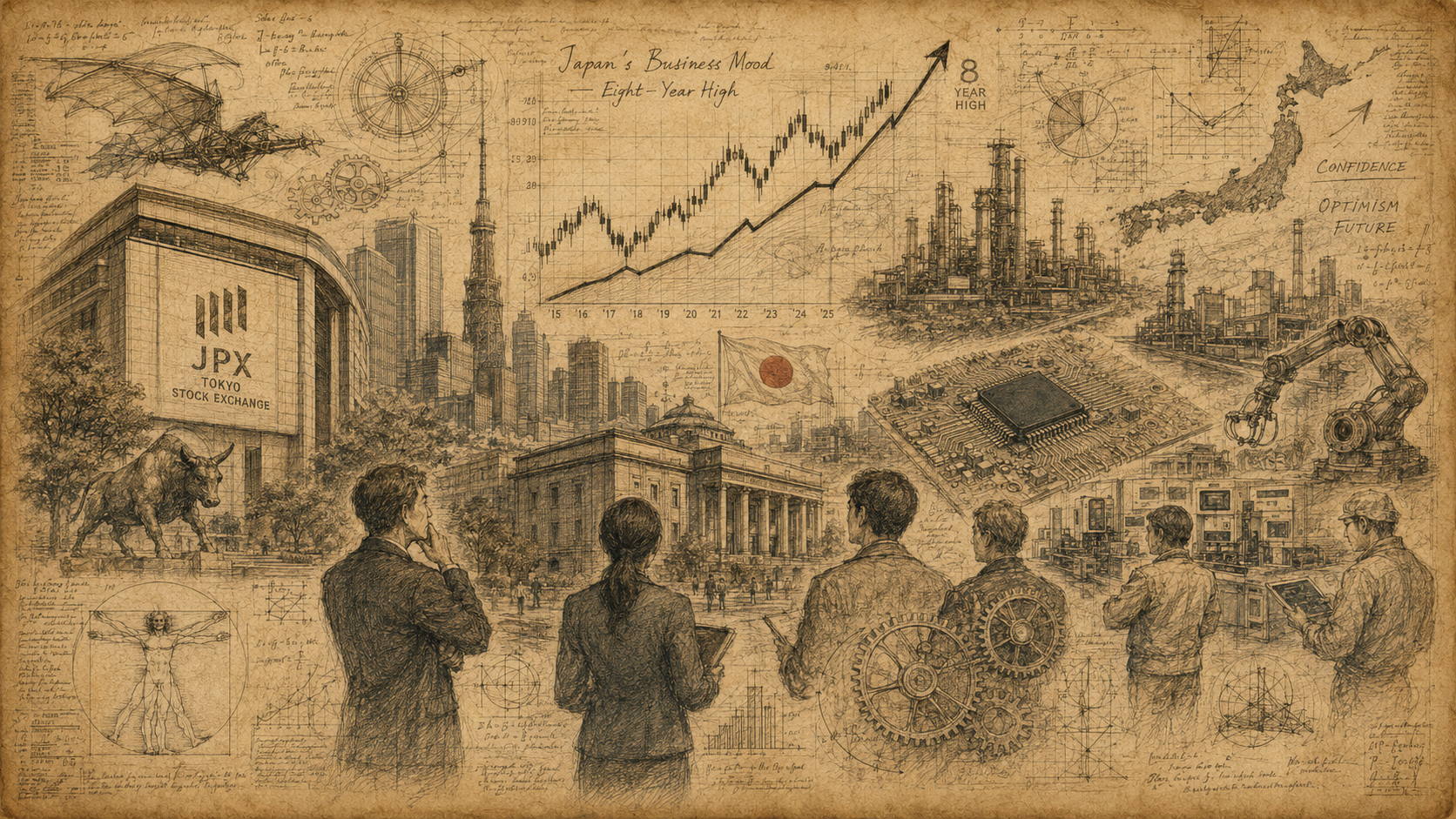

Something has shifted in the Japanese economy. The Bank of Japan’s June Tankan, released on July 1, showed the business conditions diffusion index for large manufacturers rising to +22 from +17 in March. Reuters called it the strongest level since March 2018 — an eight-year high. Large non-manufacturers rose from +36 to +37, a level not seen since 1991.

At first glance, the message looks simple: corporate Japan is confident again. But the real picture is more interesting. The yen is still trading in the low ¥160s against the dollar. Import costs remain painful. The Middle East shock has complicated energy prices and supply chains. Companies are raising wages. Interest rates have left the zero-rate era behind, with the BOJ lifting its policy rate to 1% in June. And yet business sentiment improved. That is why this Tankan matters. It is not a clean “boom” story. It is a story of companies pushing forward while still surrounded by risk.

The Tankan is one of Japan’s most important economic instruments. The June survey was conducted from May 28 to June 30 and covered 9,141 enterprises, with a 99.4% response rate. It asks firms about business conditions, prices, employment, finance, capital spending, exchange-rate assumptions and inflation expectations. That makes it different from backward-looking GDP data. The Tankan is a reading of corporate Japan’s current temperature.

The numbers that matter

The +22 reading for large manufacturers beat market expectations. The +37 reading for large non-manufacturers also beat expectations and confirmed the strength of services. Tourism, hotels, restaurants, transportation, department stores and entertainment have all benefited from inbound demand and improved pricing power.

But the survey is not pure sunshine. Large manufacturers expect the September reading to fall back to +17, and large non-manufacturers see their index dropping to +28. Companies know the current moment is strong, but they also see higher costs, energy uncertainty, supply constraints, rates and currency risk ahead. The Tankan is showing strength under clouds, not confidence without fear.

What the Tankan is: Japan’s corporate stethoscope since 1957

The Tankan has a long history. According to the Bank of Japan, Japan’s first business survey was begun in 1951 by the former Industrial Bank of Japan. The BOJ took over and revised that effort, starting the Principal Enterprises Tankan in 1957. Today the Tankan — formally the Short-Term Economic Survey of Enterprises in Japan — is released quarterly and is watched closely by markets, companies and policymakers.

Its core measure is the diffusion index. The BOJ subtracts the share of firms saying conditions are “unfavorable” from the share saying conditions are “favorable.” A reading of +22 means favorable responses exceed unfavorable ones by 22 percentage points. The number is simple. But behind it are orders, prices, profits, wage plans, production schedules and management mood.

For the Bank of Japan, the Tankan is policy intelligence. If companies are confident, capital expenditure and wages are more likely to keep rising, and prices may be easier to sustain. If companies are cautious, investment can stall and inflation may fade. During Japan’s long deflationary era, the Tankan was one of the ways policymakers listened to the heartbeat of stagnation. In 2026, that heartbeat sounds different.

Why “eight-year high” matters

The last time large manufacturers’ sentiment reached this territory was 2018. That was the later stage of Abenomics, when global growth, semiconductor demand, yen weakness and inbound tourism were supporting corporate earnings. What followed was a hard detour.

Japan raised the consumption tax to 10% in 2019. The pandemic froze tourism and hammered transport, restaurants, hotels and manufacturers. Supply chains broke. Chips became scarce. Energy prices jumped. The yen weakened sharply. Import inflation squeezed households. Then wages finally began to rise, but so did interest rates. By the time the 2026 Tankan reached +22, corporate Japan had lived through pandemic shock, supply-chain disruption, energy stress, currency weakness and policy normalization.

That is why this is not just a “back to normal” number. It is an adaptation number. Japanese companies have not returned to 2018. They have reached a new place after passing through a very different world.

AI and chips: the hidden engine behind the mood

A key reason manufacturing sentiment improved is demand linked to artificial intelligence and semiconductors. The AI boom is usually told as a software story. But behind every model and data center sits a physical economy: servers, cooling systems, power equipment, wiring, chips, specialty glass, chemicals, precision machinery and inspection tools.

Japan is not the dominant consumer-platform economy of the AI age. But it remains powerful in the industrial layers beneath it. Semiconductor materials, manufacturing equipment, precision components, sensors, factory automation and power systems all connect Japan to the global AI buildout. The Tankan’s manufacturing improvement suggests that demand is flowing into actual orders, production and investment.

Rapidus and the 2-nanometer chip race, domestic data-center demand, power-grid investment, robotics, machine tools and electronic components are not separate stories. They are parts of the same industrial turn. Japan’s economy is being supported not by a loud consumer boom, but by a quieter revaluation of its manufacturing base.

Services: tourism, pricing power and the 1991 echo

The +37 reading for large non-manufacturers is especially striking because it reaches territory last associated with 1991. That historical echo matters. In 1991, Japan was entering the long aftermath of the bubble economy. In 2026, the drivers are different: inbound tourism, hotel demand, restaurants, transport, retail, entertainment and a greater willingness to pass higher costs into prices.

Tourism is no longer a side business for Japan. It is now a central service-sector force. A weak yen makes Japan cheaper for foreign visitors. Local hotels, restaurants, railway lines, airports, shops, museums and regional attractions benefit. When firms can charge more and still retain demand, earnings improve.

But strength brings side effects. Overtourism, crowded transport, hotel shortages, labor constraints, two-tier pricing debates, municipal taxes and cultural-site preservation are all part of the same story. The non-manufacturing Tankan number is a vote of confidence in Japan’s attractiveness. It is also a warning that tourism policy must become more sophisticated.

Wages have changed the psychology

The 2026 wage round is crucial to understanding the Tankan. Rengo’s final tally showed average wage hikes of 5.01%, the third straight year above 5%. The previous two years were 5.10% and 5.25%. For Japanese companies, wage growth is no longer a one-off shock. It is becoming part of the planning environment.

For decades, Japan’s deflationary psychology was built on restraint. Companies avoided price increases. Workers did not expect meaningful wage gains. Consumers resisted higher prices. Households saved because the future felt uncertain. That cycle is finally being tested by labor shortages, inflation, corporate earnings, minimum-wage targets and a tighter market for younger workers.

Higher wages can hurt companies if they cannot pass costs on. But they can also support demand. If households earn more, they can spend more. If demand holds, firms can invest. If firms invest, productivity can rise. This is the wage-price cycle the BOJ wants to see. The Tankan suggests corporate Japan is beginning to operate in that world.

Capital expenditure: corporate Japan is still attacking

One of the most important figures in the June Tankan is capital expenditure. Large companies plan to raise capital spending by 11.5% in the fiscal year ending March 2027. That is not a soft number. It means the improved mood is turning into planned action.

The investment story is broad: chips, factory automation, logistics, data centers, decarbonization, replacement of aging facilities, labor-saving equipment, software and cybersecurity. Japanese firms spent much of the post-bubble period holding cash and avoiding bold investment. But in a world of labor shortages, higher rates, geopolitical risk and supply-chain reordering, old equipment becomes a competitive liability.

The government is trying to push the same direction. Its long-term economic blueprint aims to lift real growth above 1%, target nominal growth above 3%, and channel more than ¥370 trillion in combined public and private investment through fiscal 2040. The Tankan’s capex number suggests that at least some of that investment turn is already appearing inside corporate plans.

The weak yen: blessing and burden

The yen remains central to the story. In the June Tankan, firms assumed an average exchange rate of ¥152.57 per dollar for fiscal 2026. In the market, however, the yen was trading around the low ¥160s in early July. That gap matters. For exporters and companies with overseas earnings, a weaker yen can lift profits. For importers, energy users and households, it raises costs.

Japan imports much of its energy and food. Yen weakness feeds into gasoline, electricity, food, chemicals and industrial inputs. Firms can try to pass those costs on to customers, but there is a limit. If they pass too much on, demand can suffer. If they do not pass enough on, margins suffer. The Tankan’s strength sits on top of this delicate balance.

That is why the survey gives the BOJ a difficult signal. Strong business sentiment and high inflation expectations support rate hikes. But imported-cost inflation can also squeeze households and weaken real demand. Raise rates too little, and the yen may remain under pressure. Raise too much, and investment could slow. This is the tightrope of Japan’s second half of 2026.

Inflation expectations: the end of deflation psychology?

The Tankan showed companies expecting general prices to rise 2.7% one year ahead and 2.6% three and five years ahead. That is above the BOJ’s 2% target. The message is clear: companies no longer assume Japan will automatically return to near-zero inflation.

This is historically important. Deflation was never only a price statistic in Japan. It was a psychology: companies feared price hikes, consumers expected discounts, workers stopped expecting wage growth, and managers planned cautiously. If firms now assume inflation in the mid-2% range, that psychology is changing.

But inflation alone is not success. For higher prices to become healthy, wages, productivity, investment and consumption must move together. Prices rising without wage gains create resentment. Wages rising without productivity squeeze profits. Investment without demand wastes capital. The Tankan matters because it lets us see all those moving parts at once.

Japan.co.jp view: not “Japan is back,” but “Japan is being redesigned”

It is tempting to call this a “Japan is back” moment. Japan.co.jp would frame it differently. This is not a simple comeback. It is a redesign. The old model of cheap yen, cheap wages, cheap money and cheap prices is ending. The new model requires higher wages, higher prices, higher investment, tourism management, AI-era industrial strategy and labor-saving productivity.

The +22 Tankan reading is a number from the middle of that transition. It is strong, but it is not carefree. It is bright, but it is shadowed by currency risk and imported inflation. It is investment-led, but small firms still face pressure. It is supported by tourism, but local capacity is under strain. It is powered by AI demand, but AI infrastructure needs electricity, land, chips and engineers.

Still, the number means something. After decades of caution, Japanese companies are again acting as if the future exists. They are planning investment. They are raising wages. They are changing prices. They are selling into global demand. They are adapting.

The summer of 2026 is hot. The yen is weak. Rates are higher. The world is unstable. And yet Japan’s business mood is at an eight-year high. That contradiction is the story of the Japanese economy now.

Reader’s guide

| Question | Answer |

|---|---|

| What happened? | The BOJ’s June 2026 Tankan showed large manufacturers’ sentiment rising to +22, the strongest level since 2018. |

| Why does it matter? | AI demand, semiconductors, tourism, price pass-through and wages are supporting corporate confidence. |

| What is the warning? | Companies expect conditions to worsen by September, and yen weakness, fuel costs, rates and supply risks remain serious. |

| Historical context | The Tankan began under the BOJ in 1957 and has become one of Japan’s most important corporate sentiment surveys. |

| Japan.co.jp view | This is less a simple revival than a redesign of Japan’s wage, price, investment and industrial model. |

Sources and references

This article draws on the Bank of Japan’s June 2026 Tankan, BOJ background material on the survey, Reuters, Associated Press, Rengo wage-round reporting and exchange-rate sources.

- Bank of Japan: Tankan Outline, June 2026.

- Bank of Japan: FAQ on the Tankan and its history.

- Reuters: Japan business mood hits eight-year high.

- Associated Press: Survey shows Japan business sentiment improving for a fifth straight quarter.

- Reuters: Japan wage hikes top 5% for third year.

- Wise: USD/JPY exchange-rate history checked for July 2026.