A growth strategy for an industry that has shrunk

On June 5, 2026, Japan’s Cabinet approved the FY2025 Fisheries White Paper. Under the Fisheries Basic Act, the government reports annually to the Diet on the condition of fisheries and the measures it has taken. This edition devotes its special feature to “measures toward making aquaculture a growth industry”—from selective breeding and exports to eel conservation, full-cycle culture and land-based farms.

The choice is understandable. Wild catches face ecological limits and shifting seas; the fishing workforce is aging; domestic consumption is declining; and seafood buyers want standard sizes, scheduled delivery and stable prices. A farm can plan a harvest in a way a purse seiner following a migrating school cannot. Government shorthand calls those advantages the “four constants”: consistent quality, quantity, price and timing.

But the first chart complicates the slogan. Japanese aquaculture reached about 1.43 million tonnes in 1988, then declined to approximately 830,000 tonnes in 2024. Its share of national fisheries output has stayed in the 20% range rather than surging. “Growth” in the white paper is therefore a policy direction, not a description of the recent volume trend. It means improving value, profitability, resilience, productivity and overseas demand—not merely filling more cages.

The 23%–44% paradox

Japan produced 3.64 million tonnes of fishery and aquaculture products in 2024, down 190,000 tonnes, or 5%, from the previous year. Marine capture fisheries accounted for 2.79 million tonnes; marine aquaculture for 800,000; and inland fisheries and aquaculture for roughly 50,000. Aquaculture’s combined 830,000 tonnes was about 23% of the total.

Value tells the opposite story. Total fisheries production value was ¥1.6297 trillion. Marine aquaculture generated ¥607.7 billion and inland aquaculture ¥116.3 billion: together ¥724.0 billion, or about 44%. Marine finfish farming alone was worth ¥328.4 billion; shellfish ¥117.4 billion; and algae ¥151.8 billion. Farmed seafood carries nearly twice the share in value that it does in weight.

| Japan, 2024 | Production volume | Production value | What it shows |

|---|---|---|---|

| All fisheries and aquaculture | 3.64 million t | ¥1.6297 trillion | National baseline |

| Marine aquaculture | 800,000 t | ¥607.7 billion | Fish, shellfish and algae at sea |

| Inland aquaculture | About 30,000 t | ¥116.3 billion | Eel and other high-value production lift value share |

| All aquaculture | About 830,000 t / 23% | ¥724.0 billion / 44% | Strategic weight exceeds tonnage |

Weight comparisons need care: seaweed is reported as wet weight and shellfish with shells, while the market value includes products with very different edible yields. Even so, the broad point survives. Japan is not trying to beat commodity carp or shrimp producers on tonnes alone. It is trying to sell a reliable, differentiated product—yellowtail cut to specification, disease-screened seed, branded sea bream, scallops, pearls and, eventually, technologies and genetics.

The world farmed more; Japan did not

The global backdrop makes Japan’s contraction striking. FAO’s 2026 assessment puts total fisheries and aquaculture production at about 235 million tonnes in 2024. Aquaculture, including algae, contributed roughly 141 million tonnes; farmed aquatic animals alone crossed 100 million tonnes and exceeded capture fisheries. Wild output has remained broadly within a narrow range since the late 1980s while farming drove growth.

Most of that expansion occurred in Asia, especially China, India, Indonesia and Vietnam, with freshwater carp, tilapia, catfish, shrimp and seaweed. Japan’s industry has another structure: roughly 34% finfish, 33% algae and 32% shellfish by volume in 2024. Yellowtail is the dominant farmed fish, accounting for around half of finfish aquaculture. Geography, wages, coastal competition, typhoon exposure and a mature domestic market all constrain scale.

Japan’s seafood demand has also moved backward. Per-person consumption of edible fish and shellfish fell from 40.2 kilograms in fiscal 2001 to 21.3 kilograms in fiscal 2024. Food-fish self-sufficiency, 113% in 1964, was 52% in 2024. A shrinking, aging population makes domestic volume growth difficult; this is why the white paper repeatedly turns from the Japanese dinner table to export markets.

From Edo carp ponds to the first yellowtail farms

Aquaculture in Japan is centuries older than the present strategy. The white paper traces carp culture, oyster cultivation and nori production to the Edo period. Nori growers in Edo Bay learned to collect spores on brushwood, and sheet-making methods borrowed from Japanese paper helped turn seaweed into a transportable food. These were managed ecosystems, not sealed factories: tide, nutrients, temperature and communal coastal rules remained decisive.

In the Meiji era, inland techniques advanced for rainbow trout and eel. Hanging culture expanded for shellfish. In 1893, Kokichi Mikimoto and his collaborators achieved cultured pearls in the Toba–Shima region, a breakthrough that linked marine husbandry, craft and global luxury markets. Later methods produced round pearls and made the Akoya industry internationally famous.

Modern finfish aquaculture began with an improvised experiment. In 1928, Wazaburo Noami used a sheltered salt pond at Adoike in Hiketa, Kagawa Prefecture, to rear wild-caught juvenile yellowtail. Kagawa recognizes it as the world’s first successful commercial yellowtail culture. After wartime interruption, net-pen techniques spread in the high-growth decades, particularly for yellowtail and red sea bream. Better feed, seed transport, cold chains and coastal infrastructure turned local trials into an industry.

| Period | Milestone | Long-term significance |

|---|---|---|

| Edo period | Carp, oysters and nori cultivated; sheet nori developed | Food production tied to managed waters and local knowledge |

| Meiji era / 1893 | Trout and eel techniques advance; cultured pearl breakthrough in Toba–Shima | Hatchery science and marine luxury exports emerge |

| 1928 | Noami’s yellowtail culture succeeds at Adoike, Kagawa | Beginning of commercial Japanese marine finfish farming |

| Postwar–1988 | Net pens, formulated feeds and cold chains expand; output peaks | Aquaculture becomes a major coastal industry |

| 2020–21 | Growth Industrialization Strategy adopted, then expanded to shellfish and algae | “Market-in,” exports and integrated value chains become policy |

| 2023–26 | Land-farm notification, food-tech policy and aquaculture white-paper theme | Technology and resilience move to the center |

The strategy began in 2020, not this June

The 2026 white paper is an annual report and policy narrative, not a new aquaculture law. Its architecture comes chiefly from the Comprehensive Strategy for the Growth Industrialization of Aquaculture, adopted in July 2020 and broadened in July 2021 to cover shellfish and algae. The strategy calls for a shift from “product-out”—producing first and finding a buyer later—to “market-in,” designing production for identified customers and prices.

It also tries to join a fragmented chain. Seed producers, breeders, feed companies, farms, processors, logistics operators and retailers are expected to coordinate data, specifications and investment. Five enterprise models offer different forms of integration. This can reduce mismatch and waste, but it also changes power. A small farm tied to one buyer or genetics supplier may gain stability while losing bargaining room. The white paper highlights success cases; it is not an independent audit of every contract.

The production and export goals frequently attached to the current white paper are inherited 2030 targets from that earlier strategy. They should not be mistaken for new promises issued in June 2026, or for achievements already reached.

| Strategic item | 2018 baseline | 2030 production target | 2030 export-value target |

|---|---|---|---|

| Yellowtail group | 140,000 t; ¥16bn exports | 240,000 t | ¥160bn |

| Red sea bream | 60,000 t; ¥5bn exports | 110,000 t | ¥60bn |

| Bluefin tuna | 20,000 t | 20,000 t | Not specified in this table |

| Salmon and trout | 20,000 t | 30,000–40,000 t | Not specified in this table |

| New species, including grouper | Near zero | 10,000–20,000 t | Not specified in this table |

| Scallop | 170,000 t; ¥47.7bn exports | 210,000 t | ¥115bn |

| Pearls | ¥13.6bn production value in 2014 | ¥20bn value by 2027 | ¥47.2bn by 2030 |

The gaps are deliberately large. Yellowtail exports would need to rise tenfold from the strategy’s baseline, and production by more than 70%. The targets were set before recent feed inflation, a weak yen’s effect on imported inputs, and the 2025 mass-mortality events. A credible 2030 scorecard must publish current species-by-species output, margins and certified volume—not simply repeat the destination.

Exports are the escape route from a shrinking table

Japan imported 2.08 million tonnes of fishery products worth ¥2.1454 trillion in 2025. The weak yen and global competition for seafood raise input and import costs, yet the same exchange rate can make Japanese exports more competitive. This asymmetry helps explain the focus on brands, processing and overseas distribution.

The white paper’s examples sell control. Uwajima’s Date Maguro is slaughtered and chilled rapidly, carries Aquaculture Eco-Label certification, and has cultivated the United States market and trademark over more than a decade. Farmed yellowtail can now command a higher average price than wild yellowtail because buyers can order size, fat content and timing. Ornamental koi offer an extreme high-value example: exports to the United States rose from about ¥1.2 billion in 2024 to ¥2.7 billion in 2025, according to the white paper.

Certification is expanding but still partial. As of March 31, 2026, Japan had 20 ASC-certified operations covering 45 farms and 216 chain-of-custody operators. The government estimates ASC coverage at about 1.3% of aquaculture production. Marine Eco-Label Japan covers a broader mix of fisheries and aquaculture and is estimated at about 12%; the scopes overlap and the percentages cannot simply be added. Labels can verify rules, not guarantee that every ecological or labor trade-off has vanished.

Seed: domestication is still unfinished

A farmed fish can still begin in the wild. Japanese yellowtail farms traditionally capture mojako, juveniles that shelter beneath drifting seaweed. Only about 20% of yellowtail seed is artificially produced, the white paper says. Bluefin tuna farms also include operations that fatten wild-caught juveniles, while eel farming remains overwhelmingly dependent on wild glass eels.

Artificial seed gives breeders control over health, timing, growth, body shape and feed efficiency. Family selection and genomic information can shorten improvement cycles; disease-resistant lines may reduce losses and medicine use. The government’s 2050 Green Food System aspiration is to make Japanese eel, bluefin tuna and other aquaculture seed entirely artificial and to shift fish feed entirely to compounded formulations that reduce pressure on wild resources.

That is a direction, not a guarantee. Hatcheries can narrow genetic diversity if too few parents dominate. Patented lines may concentrate ownership. Escaped animals can interact with wild populations. Genome-edited red sea bream and pufferfish have already entered Japan’s food market through a company case highlighted in the white paper; speed and yield do not settle questions about traceability, welfare, consumer acceptance or ecological containment. Good breeding policy needs genetic monitoring and transparent rules as much as faster growth.

Feed is aquaculture’s largest bill—and its hidden fishery

Feed represents around 70% of marine finfish farming costs, according to the white paper. Fishmeal and fish oil remain important because carnivorous species need concentrated protein, lipids and omega-3 fatty acids. Japan imports much of its fishmeal, exposing farmers to Peruvian anchoveta catches, global livestock and aquaculture demand, shipping, war-related commodity disruption and exchange rates.

This is the central paradox of fed aquaculture. A cage can make the final harvest predictable, but it may still depend on variable wild fisheries upstream. Feed-conversion ratios have improved and trimmings can be recycled, yet poor sourcing can transfer fishing pressure rather than remove it. Seaweed and bivalves need no manufactured feed, but they face their own limits: water temperature, salinity, nutrients, disease and carrying capacity.

Research is testing soybean and other plant proteins, black soldier fly larvae, single-cell ingredients and microalgae. One white-paper case combined insect larvae and microalgae in feed for red sea bream and obtained growth comparable to a control diet. That is promising experimental evidence, not proof that a cheap national supply exists. Scaling requires safe raw materials, stable nutrient profiles, palatability, processing capacity and a price below volatile fishmeal.

In December 2025, the government put ¥23.2 billion into a safety-net fund for fuel and feed price surges. Insurance can prevent a temporary shock from bankrupting a farm. It cannot turn a structurally expensive feed system into an efficient one.

Warm water turned the risk chapter into a warning

The white paper arrived after a traumatic 2025. Oysters died in large numbers in Hiroshima, Okayama and Hyogo in the Seto Inland Sea. Scallops suffered mortality in Mutsu Bay, Aomori. Investigations considered combinations of sustained high temperature, high salinity, oxygen stress and food shortage rather than one universal cause. In Mutsu Bay, midwater temperatures remained above 26°C, a threshold associated with high scallop mortality risk.

Nori growers face delayed autumn starts as water remains warm and shortened harvest seasons; drought and low nutrient inflow can cause poor color. Finfish farms confront harmful algal blooms, oxygen depletion and pathogens whose ranges and severity shift with temperature. Japan’s 2024 white paper had already made ocean change a major theme. The 2026 edition shows that climate adaptation is not a separate environmental chapter—it is farm economics.

Countermeasures include denser monitoring, early warnings, moving or submerging cages, aeration, changing harvest calendars, selective breeding and insurance riders. Red-tide-resistant yellowtail research found wide survival differences among families; in a next-generation trial, one selected cross survived at 42% against 25% for a control. Useful as that signal is, both groups still lost many fish. Resistance is relative, and a line selected against one bloom organism may not solve heat, disease or another toxin.

| Risk | Promoted response | What remains |

|---|---|---|

| Red tide / low oxygen | Sensors, forecasts, cage movement or submergence, aeration, resistant lines | Forecast uncertainty; equipment and relocation costs; multiple bloom species |

| High water temperature | Species and site shifts, earlier harvest, offshore/deeper water, breeding | Heat can exceed biological thresholds across a whole region |

| Disease | Vaccines, screened seed, remote diagnosis, biosecurity | Warmer seas and imported seed can alter pathogen risk |

| Feed and fuel prices | Alternative ingredients, efficiency, government safety net | Imported inputs and yen exposure remain |

| Storms / equipment failure | Stronger or submersible pens, insurance, remote control | Typhoons, worker safety, escapes and catastrophic losses |

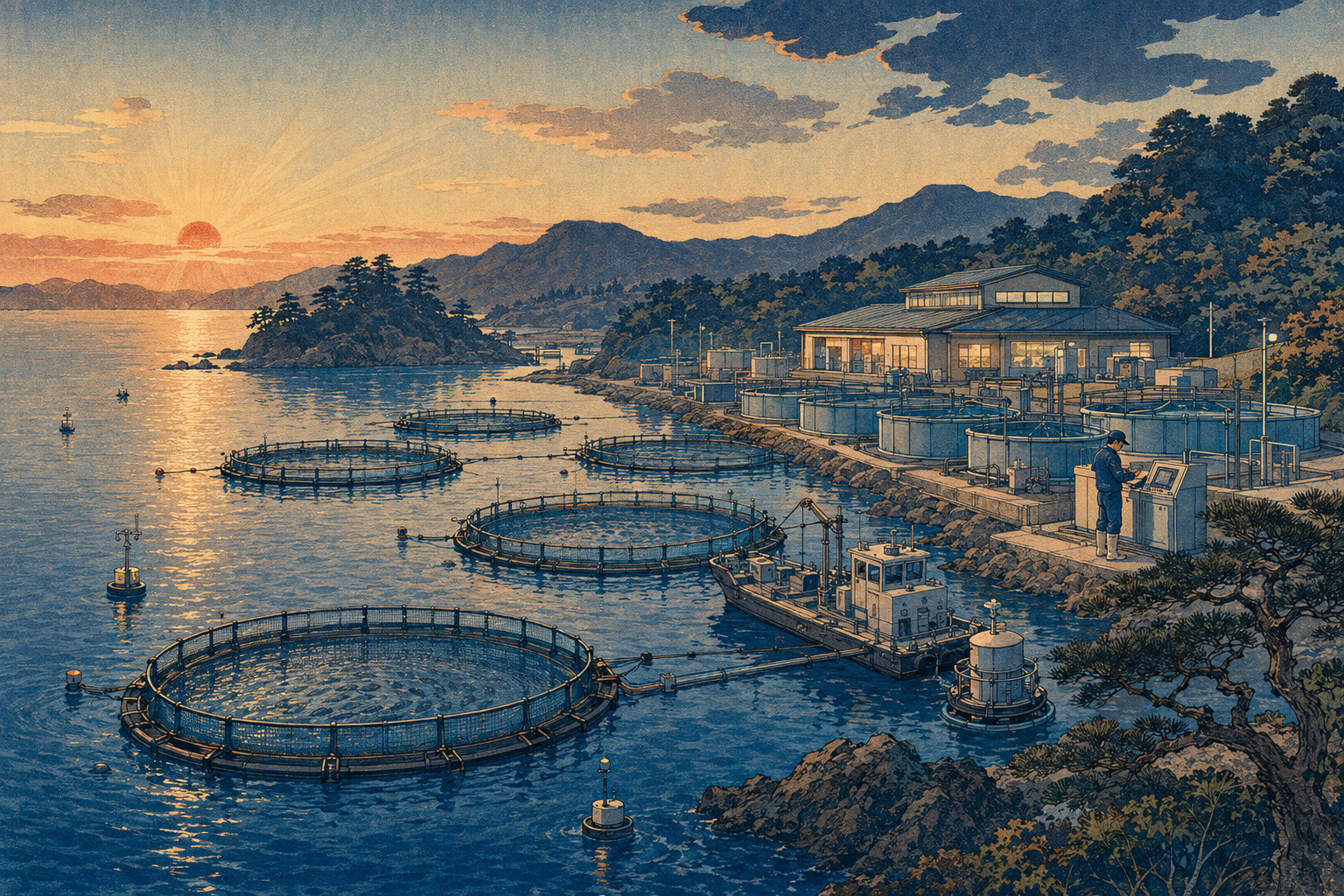

Offshore and smart farms change labor, not biology

Fish farming is physically hard, weather-dependent work, often far from major cities. Automatic feeders, biomass cameras, environmental sensors, AI-assisted appetite estimation, net-cleaning robots and remote monitoring can reduce boat trips and feed waste. At an Ainan, Ehime operation cited in the white paper, output grew from about 600,000 fish in 2000 to 1.7 million in 2024 alongside workplace improvements.

Moving offshore offers stronger currents that disperse waste and may reduce some red-tide and coastal water-quality exposure. A 2021–2025 demonstration off Kushima, Miyazaki, used large submersible cages, a feed vessel capable of carrying 25 tonnes and robotic net cleaning. Scale can spread fixed costs and meet large contracts.

It also creates new concentration risk. Offshore hardware, service vessels, telemetry and moorings demand heavy capital. Distance raises repair and emergency costs; waves and typhoons test systems; a failure can release many fish at once. Digital control requires communications and cybersecurity. Automation may make work safer, but coastal communities will judge the strategy by durable local income and skills, not the number of sensors purchased.

Disease losses fell, but did not disappear

Fish-disease damage was estimated at ¥11.3 billion in 2023, around 3% of aquaculture production value. That is far below the roughly ¥30 billion peak in 1994–95, reflecting vaccines, husbandry and diagnosis. It is still a significant annual loss, and aggregate percentages conceal farms that lose an entire cohort.

Higher temperatures can accelerate pathogens or stress fish. Importing seed adds routes of entry. Crowded populations make transmission efficient. Antimicrobials can select resistance that matters to animal and human health. The sensible hierarchy is prevention first: healthy and diverse seed, vaccination where available, lower stress, appropriate density, fallowing, disinfection, mortality reporting and rapid diagnosis. Drugs remain a tool, not a substitute for system design.

The eel test: what “full-cycle” really means

Eel culture exposes the distance between farming and domestication. Commercial farms buy glass eels captured from the wild, raise them to market size and do not close the reproductive cycle. Japanese eel abundance and opaque international trade have made seed supply a conservation and enforcement problem. Japan licenses eel culture, caps stocking, cooperates regionally and has strengthened traceability and rules against illegally caught glass eels.

Full-cycle aquaculture means captive-bred parents produce eggs; larvae become glass eels and adults; and some of those adults become the next broodstock. Japanese researchers have achieved the biology. Economics remains severe. From the 2012–2021 fishing seasons, wild glass eels cost roughly ¥180–¥600 each; an artificially produced seed cost about ¥1,800 in 2023 even after large reductions.

A patented cylindrical tank reported in the white paper raised roughly 1,000 glass eels per tank, versus 20–80 in the older system, and helped bring rearing cost to about one-twentieth of its former level. Automation, survival, broodstock quality and mass production still need work. “Full-cycle achieved” does not mean supermarket eel is now independent of the wild.

At CITES CoP20 in 2025, a European Union proposal to place all Anguilla eels in Appendix II failed, 35 votes to 100, while parties adopted a consensus eel-conservation resolution. Japan argued that the listing criteria were not met and that existing regional measures should be strengthened. Rejection of a trade listing is not a finding that eel populations are secure. The technology case and the conservation case must be assessed together.

Land-based farming is visible, but still tiny

Land systems promise control over temperature, disease entry, water quality, escapes and proximity to consumers. Flow-through farms use large volumes of new water; semi-closed systems reuse part of it; recirculating aquaculture systems filter and reuse most water. Japan introduced a notification regime for certain land-based farms in April 2023 because regulators needed to know where these new operations were and how their effluent might affect surrounding waters.

As of January 1, 2026, the Fisheries Agency had received 808 notifications, each representing a facility. Okinawa led with 195, followed by Oita with 53 and Kagoshima with 36. The most frequently listed products were sea grapes, flounder and kuruma prawn. The counts include facilities listing species they plan to farm and double-count species at multi-species sites, so they are not production totals.

Actual land-based output in 2024 was about 7,000 tonnes—roughly 0.8% of Japanese aquaculture. High construction and electricity costs remain the barrier. A recirculating system exchanges ecological exposure for pumps, oxygenation, filtration, heat control and backup power. Waste nutrients still need disposal or reuse. A short electrical or biofilter failure can become a mass-mortality event.

Novel products show the possible range. A land nori project produced about 100 kilograms of dried seaweed, around 30,000 sheets, in 2025 and is testing a distributed model aimed at two million sheets a year. The case is a pilot, not proof of national scale. Japan added land-based flounder to mutual-aid insurance from FY2026, a small but practical sign that policy is moving from demonstrations toward business risk.

Aquaculture is not automatically sustainable

Replacing a wild catch with a farmed fish can reduce pressure on one stock, but sustainability depends on the system. Finfish cages release nutrients and feces; excessive density can degrade the bottom. Feed may contain wild fish, soy or other ingredients with distant ecological footprints. Escapes can spread disease or genes. Chemicals and antibiotics require restraint. Farms compete for bays with capture fishers, tourism, shipping, conservation and residents.

Bivalves and seaweeds can provide habitat and remove nutrients, but large operations alter ecosystems and remain vulnerable to heat and poor water quality. Offshore dispersal can prevent a local concentration while making impacts harder to measure. Land-based systems can contain fish but consume electricity and concentrate sludge. No method earns a green label merely by changing its address.

Better measures would report survival, feed-conversion and fish-in/fish-out ratios, medicine use, escapes, benthic condition, greenhouse-gas intensity, water use, worker safety and profitability per farmed species. Certification and traceability can help, but public data are needed to tell an innovation story from a durable improvement.

What would make the bet succeed?

First, Japan has to protect the biological base: healthy broodstock, genetically diverse artificial seed, disease surveillance, climate-ready siting and transparent mortality reporting. Second, it must lower the resource bill: better feed conversion, responsibly sourced ingredients, alternatives that work at commercial scale, and energy efficiency in land systems. Third, it needs markets willing to pay for quality and verified practice—not just temporary support from a weak yen.

Fourth, gains must reach coastal producers and workers. Integrated supply chains can finance technology and guarantee buyers, but contracts need fair risk sharing. Insurance should encourage prevention rather than socialize repeated failure. Public research should retain accessible breeding and husbandry knowledge even as companies protect genuine inventions.

Finally, targets need annual progress measures. The inherited 2030 table is useful only if the public can compare it with current output, export value, margins and environmental performance. The white paper is a government account of its policies and selected examples; it should be read alongside statistics, farm-level evidence and independent ecological review.

The future is a portfolio, not one perfect farm

Japan will not solve seafood security with a single technology. Coastal shellfish and seaweed, improved net pens, selective breeding, hatcheries, offshore systems, recirculating tanks, wild fisheries and imports will coexist. Each shifts risk rather than abolishing it. The strongest portfolio uses the right species and system for a place, preserves options and avoids betting an entire region on one genotype, feed source or export market.

The 2026 white paper matters because it acknowledges that aquaculture now bears far more economic weight than its tonnage suggests. It also places feed, disease, climate, eel conservation and business risk inside the growth story. Its weakness is the familiar one of strategy documents: demonstrations and targets can look smoother on paper than organisms, markets and coastal communities behave in practice.

Japan’s aquaculture future is therefore neither a blue-tech inevitability nor a retreat from the sea. It is an attempt to turn centuries of aquatic husbandry into a predictable, higher-value industry under unprecedented environmental pressure. The bet will be won not when the country installs more tanks or cages, but when farms can survive, ecosystems can absorb their presence, consumers can trust the product and the numbers improve without hiding the costs.

Sources and further reading

- Fisheries Agency, “FY2025 Fisheries White Paper released” (June 5, 2026): Cabinet approval, statutory status and special theme.

- Fisheries Agency, FY2025 Fisheries White Paper, full index: complete and chapter PDFs, including reference materials.

- Special feature: Measures toward making aquaculture a growth industry: history, production structure, strategy, breeding, feed, risk, eel and land systems.

- White Paper Chapter 1: seafood supply, consumption and trade: consumption, self-sufficiency, imports and certification.

- White Paper Chapter 2: Japan’s fishing and aquaculture industries: 2024 volume, value, employment and operating conditions.

- Ministry of Agriculture, Forestry and Fisheries, ministerial press conference (June 5, 2026): official presentation of the white paper.

- Fisheries Agency, Comprehensive Strategy for Growth Industrialization of Aquaculture: 2020 adoption, 2021 revision and supporting material.

- Revised Comprehensive Strategy, full text: market-in model, strategic species and 2030 production/export targets.

- Fisheries Agency, strategy adoption announcement (July 14, 2020): policy origin and objectives.

- Aquaculture Growth Industrialization Strategy Council: council record and item-level action plans.

- Fisheries measures under the Green Food System Strategy: 2050 artificial-seed and formulated-feed aspirations.

- Fisheries Agency, land-based aquaculture notification system: regulatory rationale and 808 facilities as of January 1, 2026.

- Fisheries Agency, marine aquaculture production by major species: official statistical definitions and historical series.

- FAO, The State of World Fisheries and Aquaculture 2026: key results: 2024 global production, capture plateau and aquaculture growth.

- FAO, SOFIA 2024 release: the earlier milestone when farmed aquatic animals first exceeded capture output.

- Kagawa Prefecture, history of hamachi aquaculture: Wazaburo Noami and the 1928 Adoike success.

- Kagawa Prefecture, yellowtail production and origins: local industry history and statistical context.

- MAFF, traditional seaweed products: Edo-period nori cultivation and sheet-making history.

- MAFF, Toba–Shima cultured-pearl heritage: the 1893 breakthrough and regional history.

- Fisheries Agency, FY2024 Fisheries White Paper release: the preceding theme of marine environmental change and adaptation.

- Hiroshima Prefecture, support related to oyster mortality: official measures following the 2025 damage.

- Fisheries Agency, Fisheries White Paper archive: editions and long-run policy record.

Editorial note: The FY2025 White Paper was approved on June 5, 2026; this article is prepared for the July 19 Marine Special. “Bet” and “growth industry” describe policy direction, not a forecast or evidence that Japanese aquaculture volume is currently rising. The 2030 figures are targets inherited from the 2020/2021 strategy, while the 2050 seed and feed objectives are aspirations under the Green Food System Strategy. Production and value figures refer to official 2024 statistics and may use different weight conventions for fish, shellfish and wet seaweed. Land-farm notifications count facilities and planned species, not output. Case studies and experimental survival results should not be generalized to the national industry without commercial-scale evidence. Currency strip: 1 US Dollar = 162.39 Japanese Yen, supplied for this edition.