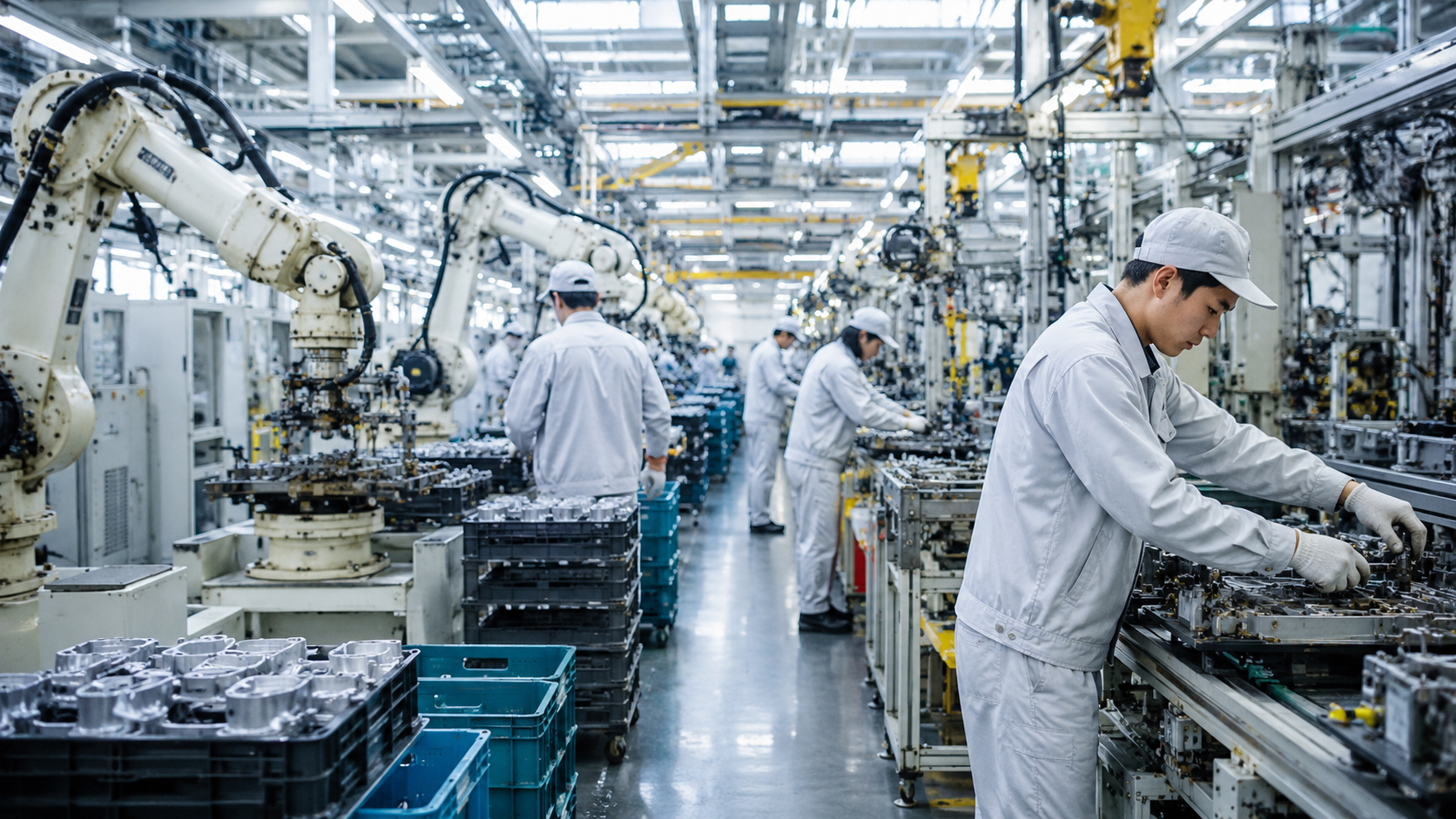

A small number, a large sound on the factory floor

Every so often, Japan’s economy announces itself not with a speech, not with a stock-market fireworks show, and not with a new slogan from Kasumigaseki, but with something quieter: a new order on a factory terminal, a purchasing manager checking component delivery dates, a shift supervisor rewriting next month’s roster.

In June 2026, that kind of morning arrived in Japanese manufacturing. Reuters reported that the flash S&P Global Japan Manufacturing Purchasing Managers’ Index rose to 54.9 from 54.5 in May. In PMI language, anything above 50 means expansion. But the more interesting story was underneath the headline number: new orders surged at the fastest pace in more than four years, while manufacturing employment grew at the quickest rate in more than eight years.

Services improved too, with the services PMI rising to 51.8 from 50.0, and the composite PMI climbing to 52.5 from 51.1. In a month when the yen was again near 160 to the dollar, energy costs were tense, and geopolitics was not exactly sending Japan a love letter, the factory data provided something the country badly needed: a positive economic counterweight.

This is not a victory parade. It is a deeper breath.

Strong economic data always comes with a warning label. June’s order surge may not be pure end-demand. Reuters noted that customer stockpiling played a role, as firms tried to guard against supply disruption and inflation linked to the Iran war. When companies fear that prices will rise or parts may become harder to source, they bring purchases forward. The factory receives a bigger order. The economy looks better. But the warehouse may simply be filling early.

That does not make the numbers meaningless. Stockpiling is itself a signal. It means customers believe risk is real, supply chains are fragile, and waiting may be dangerous. But it does mean that June should be read with discipline. A one-month surge can become a real cycle, or it can fade once inventories are rebuilt.

Japan has lived with “solid but not fast” for so long that any sign of industrial acceleration feels tempting to overstate. The right reaction is more careful: Japan’s factories are not suddenly roaring like 1988. But they are not asleep either. The machine is turning, and the sound is louder than it was.

Japan became modern through the factory

To understand why a manufacturing PMI matters in Japan, it helps to remember that the country became modern through industry. In the Meiji period, the state built railways, ports, telegraph lines, model factories, banks, and schools not as decorative reforms but as survival tools. Industrialization was how Japan tried to avoid being swallowed by the imperial powers.

Textiles, shipbuilding, steel, machinery, and later chemicals and automobiles built the bones of modern Japan. After the destruction of World War II, industry became the engine of recovery. Government, banks, corporate groups, workers, and export markets formed the architecture of the postwar miracle. MITI became shorthand for an industrial policy state that did not simply wait for markets to decide the future.

By the 1960s, 1970s and 1980s, Japan’s factories had turned into objects of global fascination and fear. Cars, televisions, cameras, stereos, machine tools, semiconductors, robotics. “Made in Japan” changed from a cheap label into a quality promise. The world bought Japanese products, and rival companies studied Japanese production.

The quiet revolution of the Toyota Production System

No history of Japanese manufacturing can avoid Toyota. Just-in-time, jidoka, kaizen, waste reduction: these concepts now live in business schools and factory manuals around the world. But they did not begin as elegant theory. They began as survival logic in a country with limited capital, limited space, and a fierce need to make every movement count.

Toyota’s idea of making only what is needed, when it is needed, in the amount needed, became one of the great industrial ideas of the twentieth century. It reduced waste, exposed problems quickly, and gave workers responsibility for quality. A good factory was not just a place where machines ran; it was a place where people thought.

Yet the same system revealed vulnerabilities in the 2020s. Just-in-time is powerful in normal conditions. But when a pandemic, earthquake, war, shipping disruption, or chip shortage removes one part, the whole line can stop. The modern lesson is not that Toyota was wrong. It is that efficiency and resilience must now be designed together.

The lost decades did not kill the factory

After the bubble burst in the early 1990s, Japan entered a long period of slow growth, deflation, financial stress, and demographic decline. Production moved abroad. China and Southeast Asia became factory floors for the world. Many Japanese towns that had grown around plants felt the pressure. Young workers looked elsewhere.

But Japanese manufacturing did not disappear. It moved deeper into the supply chain. Even where Japan lost consumer-electronics glory, it remained strong in materials, precision components, factory automation, machine tools, sensors, chemicals, and semiconductor equipment. The final product might carry another country’s brand, but the hidden parts often carried Japanese engineering.

That hidden strength matters in 2026. AI, electric vehicles, data centers, defense systems, medical devices, renewable energy, and advanced chips all require materials, components, precision tools, and disciplined production. Japan may no longer dominate every shiny consumer device, but it still holds many of the screws behind the stage.

Semiconductor demand is brightening machinery and chemicals

The June Reuters Tankan also showed manufacturers’ sentiment improving for a second month, helped by chip-related demand. That matters because semiconductors are not only chips. They are chemicals, gases, wafers, power systems, pumps, inspection tools, robotics, cleanroom components, logistics, and skilled labor.

Japan’s government has made chips a central economic-security priority. Rapidus, TSMC-linked investment in Kumamoto, subsidies, and plans to multiply domestic semiconductor sales by 2040 all point in the same direction: Japan wants to restore a deeper role in the chip world, not simply because chips are profitable, but because they are now infrastructure.

The challenge is huge. Taiwan, South Korea, the United States, China, and Europe are all spending aggressively. Japan lacks enough skilled workers. Advanced fabs need power, water, land, and extreme execution discipline. But Japan’s strengths — materials, equipment, precision, quality culture, and industrial patience — match many of the hardest parts of the semiconductor chain.

The weak yen: tailwind and knife edge

A weak yen is never just good or bad for Japanese factories. For exporters, it can boost profits when overseas earnings are translated back into yen. It can improve price competitiveness. But factories also import energy, metals, chemical inputs, food-related materials, machinery, and components. A weak yen raises those bills.

That is why June’s manufacturing data is complicated. Orders are up. Hiring is stronger. But input costs remain painful. The Iran war has added energy and raw-material stress, and the yen near 160 makes imported inflation harder to ignore. A manufacturer can receive more orders and still worry about margins.

The result is an economy with both encouragement and strain. The machine is moving, but belts are under tension. If firms can pass on costs, protect margins, raise wages, and invest, the cycle can become healthier. If costs eat the recovery, the order surge may feel better in surveys than in profit statements.

For regional Japan, this is not an abstract data point

In Tokyo, PMI is a number. In regional Japan, it is a lunch counter, a commuter train, a machine-tool supplier, a technical high school, a truck route, a town budget. Automotive parts in Aichi, precision machinery in Nagano, electronics in Tohoku, chemicals in Kyushu, machine tools in Shizuoka, industrial clusters around ports and rail lines — manufacturing is a local economy.

When new orders rise, overtime may return. Suppliers may receive calls. Temporary workers may be brought back. A factory cafeteria serves more meals. A small restaurant near the station gets a few more customers. Economic indicators are really collections of ordinary lives.

For Japan to regain confidence, the Nikkei alone is not enough. Regional factories must offer young people wages, skills, pride, and a connection to the industries of the future. A manufacturing revival that does not reach regional towns will be too narrow to change the country’s mood.

Monozukuri must stop being nostalgia

Japan loves the word monozukuri. It can mean craft, making, discipline, quality, and pride in production. At its best, it is beautiful. At its worst, it becomes nostalgia: old factories, old craftsmen, old glory, old Japan.

In 2026, monozukuri cannot be a museum word. It must mean AI-assisted factories, robot-human collaboration, advanced materials, low-carbon production, chips, batteries, medical devices, space components, defense supply chains, and resilient logistics. The old strengths must be wired into new industries.

That requires investment, not sentimental speeches. It requires better wages, not only better slogans. It requires training, power supply, land, industrial zoning, faster permitting, and managers willing to stop treating cash like a shrine object. Japan has the factory culture. The question is whether it can give that culture a future.

What would make June real?

So, are Japan’s factories finally waking up? The honest answer is: partly yes, not yet fully. The June PMI, new orders, employment growth, and composite improvement are genuinely positive. They show that the economy is breathing more deeply.

But a true revival needs four things. First, orders must continue after stockpiles are rebuilt. Second, firms must turn demand into wages and capital investment. Third, chip and AI-related demand must spread beyond a handful of large names into mid-sized suppliers. Fourth, the weak yen must become a reason to invest at home, not just an accounting gift to exporters.

Japan’s factories do not wake like a stadium crowd. They wake like machines: checked, oiled, listened to, and gradually brought up to speed. June’s data sounds like the first good noise.

That noise is not glamorous. It is not a World Cup goal. It is not a stock-market rocket. It is the hum of a line, the click of inspection tools, the movement of parts bins, the warning beep of a forklift, the quiet confidence of a supervisor who has enough orders to worry about tomorrow.

In June, Japan’s factories opened their eyes. The next question is where they look.

- The June manufacturing PMI rose to 54.9, signaling faster expansion.

- New orders grew at the fastest pace in more than four years, while employment rose at the quickest pace in more than eight years.

- Stockpiling may have boosted the numbers, so sustainability is the key question.

- Chip demand, the weak yen, high input costs, and Middle East instability are creating both tailwinds and headwinds.

- A true revival must turn orders into wages, capital investment, regional jobs, and next-generation industrial capacity.

Sources and references

This article draws on Reuters reporting on Japan’s June 2026 manufacturing PMI, the Reuters Tankan, S&P Global / au Jibun Bank PMI information, Toyota’s official description of the Toyota Production System, and Reuters reporting on Japan’s semiconductor strategy.

- Reuters: Japan's factory activity expands at faster pace in June as new orders surge

- Reuters: Japan manufacturers' sentiment rises for second month on chip-driven demand

- Reuters: Japan's factory growth slows as cost pressures surge

- Reuters: Japan factory activity returns to growth after seven months

- Toyota: Toyota Production System

- Toyota: Basic concept of the Toyota Production System

- Reuters: Japan approves additional support for Rapidus

- Reuters: Japan targets fivefold rise in domestically made chip sales by 2040